Weekly Strategy Update

Posted by GBA Administrator | Misc, Weekly Strategy Market Update | No CommentsWheat; With a recent rise in FOB sales values, Western Australian new season wheat is finally priced into

Indonesian markets, all be at very tight margins. Buyers are still very much hand to mouth so appetite is

limited with a likely big WA crop on its way. Worth holding off on sales of new crop, sell old crop with

Grain95. Hard wheat the possible exception with export sales priced at +18 on APW1 and WA to unlikely

see much of it this year.

Barley; Very similar to wheat. Western Australian barley is now nearly at export parity into some markets

(Algeria). Not a traditional home for our barley but no complaints here. Worth holding at these levels,

especially if a high chance of malt barley.

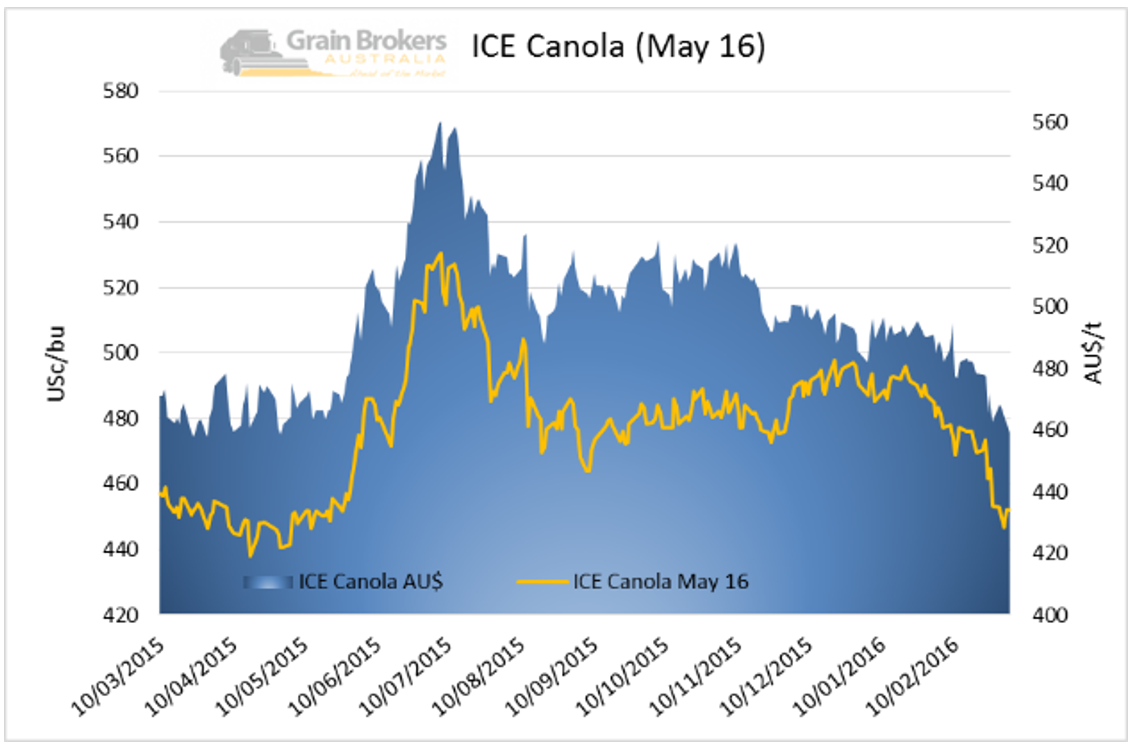

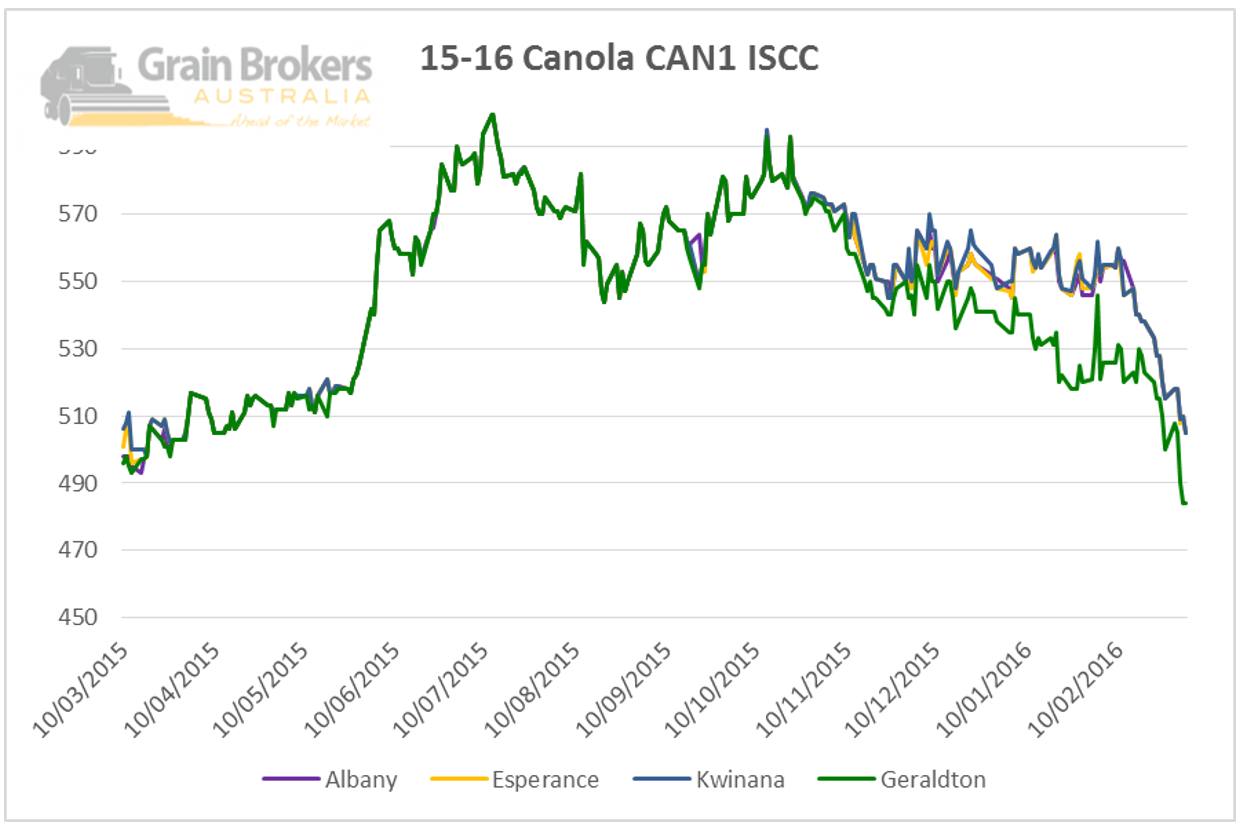

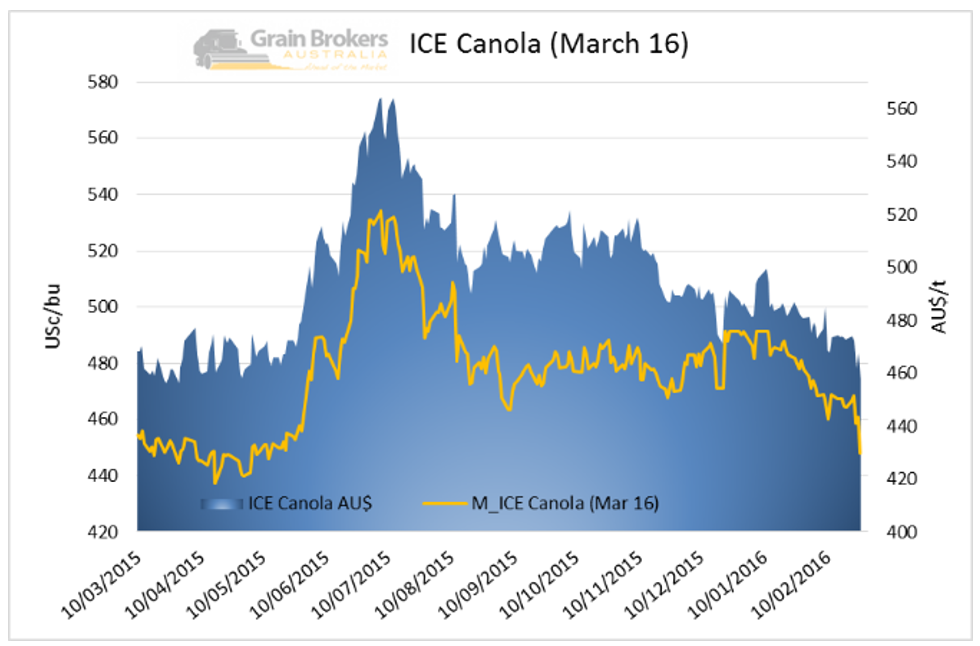

Canola; With new season canola sitting at $550 FIS all ports, this is the obvious sale for most growers.

Strong yields and lower risk of frost should see those chasing harvest cash flow being aggressive on GM

and Non GM canola. Oil demand is strong due to strong crushing margins so more upside is not out of the

question, but it is the best sale at this stage.